India is critical in the global push toward net-zero because of its large and growing energy demand. Its efforts to reduce emissions will also be a model for other emerging economies.

Published: August 3, 2023

Any path to global net-zero emissions will have to travel through India due to the country’s energy use, its projected demand growth and the commensurate increase in greenhouse gas emissions. India’s development trajectory will also influence countries in the Global South that are trying to provide secure, reliable and affordable energy to their citizens while reducing emissions. India’s policymakers and companies can use many technology, policy and finance levers to deliver the energy required to meet the nation’s economic aspirations while mitigating the impacts of climate change.

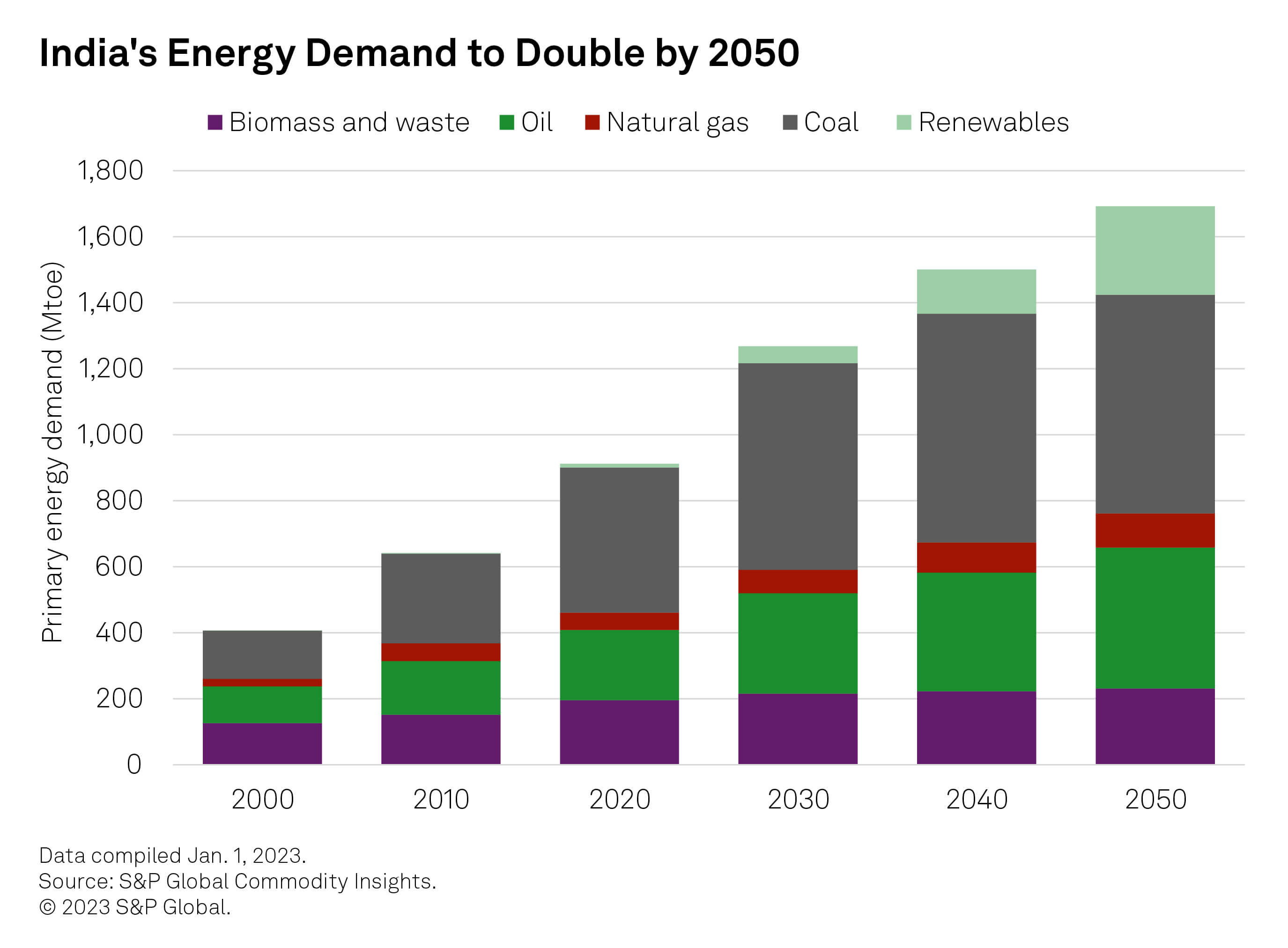

India’s energy transition reflects its robust economic growth, with a fast-expanding middle class and rapid urbanization. The nation is the third-largest consumer of energy globally, according to data from S&P Global Commodity Insights. Total primary energy demand more than doubled from 2000 to 2020, surging to 937 million tons of oil equivalent (Mtoe) from 417 Mtoe. Still, India’s energy consumption per capita is less than 1/10th of the US’s. How India meets its growing energy demand and changes its primary energy mix over the coming decade will substantially influence global energy markets and help determine if, and when, global emissions targets are reached.

India’s slogan for its G20 presidency — “One Earth, One Family, One Future” — is fitting at a time when the world is grappling with many crises simultaneously. Over the last 18 months, the focus globally has shifted to balancing energy transition with improving energy access, ensuring energy security and providing affordable energy supplies. The impact of climate change is also being felt globally and, together with high energy prices, it is accelerating the widening of the socioeconomic divide between the Global North and South. The ability of emerging economies such as India to absorb these economic shocks and to cope with extreme weather and other climate-related emergencies will have reverberations worldwide.

The ability of emerging economies such as India to absorb these economic shocks and to cope with extreme weather and other climate-related emergencies will have reverberations worldwide.

India’s economy will average 6.7% per annum GDP growth from fiscal 2024 to fiscal 2031, and its increasing energy demand will have a sustained global impact. The nation’s oil consumption will jump to 305 Mtoe in 2030 from 210 Mtoe in 2020, according to S&P Global Commodity Insights. Gas consumption will rise to 70 Mtoe from 53 Mtoe. Limited domestic supplies mean that India’s oil imports will exceed 90% of demand by 2030 at 280 Mtoe. Gas imports will surpass 60% of supplies, at 44 Mtoe. Coal will buck the trend, with imports remaining at about 25%, due to India’s own substantial resources. India already spends more than $160 billion of foreign exchange every year on energy imports, according to government statistics. The import bill is likely to double in the next 15 years without steps to reduce this import dependence. Higher imports will put a further burden on government finances.

Ensuring secure and affordable supplies of oil and gas is the highest energy priority for the government. There are several opportunities to reduce import dependence.

Upstream oil and gas: Domestic exploration has yielded mixed results over the last decade with no new major discoveries. Renewed interest in India from international oil and gas companies is likely to have limited impact because these companies are reducing oil/gas investments while transitioning to a broader fuel mix. Still, there is potential to boost output at Indian oil/gas fields using secondary and tertiary recovery technologies. Average recovery factors in India are 20%-30% compared with global averages of 35%-40%. The application of new technologies, including digital technologies, machine learning and data analytics, provides a further impetus to focus on improving recovery factors. High oil prices are another incentive for increasing domestic oil and gas production.

International assets: Many oil and gas companies around the world are divesting oil/gas assets and focusing on energy transition to meet net-zero targets. Indian public sector oil/gas companies can pool resources and jointly bid for these assets. They can also partner with strategic international investors that want to access India’s growing domestic energy market. Greater ownership of foreign oil/gas supplies will ensure energy security for India and help in managing price volatility.

Deployment of renewables: Solar photovoltaic installations have grown 12-fold in India since 2015, based on S&P Global Commodity Insights data, while wind power capacity has doubled. Further accelerating deployment of renewables will be critical in achieving the government’s target of increasing installed renewables capacity to 500 GW by 2030. This will help meet growing electricity demand while keeping prices affordable and cutting emissions. It will also reduce the impact of gas price volatility on power generation and support the retirement of old and inefficient coal power plants.

Further accelerating deployment of renewables will be critical in achieving the government’s target of increasing installed renewables capacity to 500 GW by 2030.

Hydrogen: The government launched the National Green Hydrogen Mission earlier this year with the goal of producing 5 million metric tons of the fuel annually by 2030. This will help reduce fossil-fuel imports and turn India into a leading producer and exporter of green hydrogen. The government plans to export 70% of output overseas. Domestically, hydrogen can be utilized for long-duration storage of renewable energy, as well as replacing fossil fuels in industry and heavy-duty transportation. It can also help to decarbonize India’s steel sector and make a significant impact in reducing emissions.

Any road to net-zero globally will have to travel through India. India’s economic growth coupled with rising demand for energy will result in a continuing increase in greenhouse gas emissions for the foreseeable future. The historical disparity of cumulative GHG emissions between the Global North and Global South is well acknowledged; however, effects are being felt around the world. India is seeing unprecedented temperatures, floods and droughts, as well as deteriorating air quality. Net-zero emissions targets are also likely to be superseded over the next decade by a focus on energy security and affordability.

Over the last decade, the focus has been on improving energy access via rural electrification and on ensuring affordability through targeted subsidies. Looking forward, India will have to strike a balance to increase energy access and reliability while delivering affordable energy supplies and diversifying its fuel mix to reduce the overall carbon intensity of its energy system. There are several pathways to reducing emissions.

India will have to strike a balance to increase energy access and reliability while delivering affordable energy supplies and diversifying its fuel mix to reduce the overall carbon intensity of its energy system.

Power sector: Power generation is India’s largest source of GHG emissions because coal provides over 70% of the country’s electricity. It is unrealistic to rapidly reduce coal’s share in the fuel mix, even with richer countries providing support through initiatives such as the Just Energy Transition Partnership. Nevertheless, aging and inefficient coal plants can be phased out, while newer plants can be cleaned up to meet more stringent emissions standards. The deployment of renewables can also be stepped up significantly by establishing a domestic clean-energy supply chain.

Transport sector: Decarbonizing the transport sector will likely be more challenging than decarbonizing power. The sector can start by electrifying two- and three-wheelers, which account for about two-thirds of India’s petrol demand. Deploying the infrastructure for these vehicles will be easier than setting up nationwide charging systems for light-duty vehicles. Mass transportation can also be fully electrified. Rapidly scaling up production of biofuels from agricultural waste would increase liquid fuel supply and reduce local air pollution.

Energy efficiency: A nationwide initiative to accelerate energy efficiency could pay significant dividends. Other expanding economies have shown that it is possible to slow growth in energy demand with efficiency measures, which then eases emissions. Energy savings would come from industry, buildings and transportation.

India and the rest of the world are joined at the hip in the journey to reach net-zero emissions. It will be a hollow victory if the Global North reaches net-zero and the Global South remains far behind. Developing countries will be watching closely as India continues its growth trajectory while trying to reduce the carbon intensity of its economy and ultimately bend its total GHG emissions curve. The way ahead will not be straightforward; however, there are actions that will enable the provision of secure, affordable and sustainable heat, light and mobility to the citizens of India.

Increase energy financing: The Indian government estimates that more than $10 trillion of new investments will be required to reach its goal of net-zero by 2070. Additional work will be required for capacity building, improving systemic efficiency and increasing investor confidence. The Reserve Bank of India has highlighted an urgent need for a supportive Indian green taxonomy and carbon pricing. More broadly, the International Energy Agency’s “World Energy Investment 2023” report again highlighted the huge imbalance between clean energy investments in developing and developed economies. There are immediate and timely opportunities to accelerate investments in the Global South via the G20 and COP28.

Improve policy alignment and coordination: The pace of technological and geopolitical developments affecting the global energy landscape continues to accelerate. India’s energy needs require a nimble policy and political response with coordination and alignment among multiple stakeholders, including the government, private sector and the public. IEA members such as the US and Japan could serve as a model for creating a single energy-focused entity that is responsible for coordinating national energy strategy, aligning diverse interests and accelerating decision-making.

Strengthen national champions: State-owned companies and national champions will be instrumental in delivering India’s energy and climate future. These companies will need global partnerships to access international finance and accelerate the implementation of new and emerging technologies. While progress has been made in increasing commercial focus and reducing bureaucracy, national champions need to be more agile in order to cultivate overseas partnerships, attract capital and access state-of-the-art technology. State champions can also pool resources and coordinate strategies when bidding for assets overseas.

Accelerate market orientation: Ongoing reforms have improved market-based pricing for energy, as well as enabling more efficient and transparent targeting of subsidies. More work is needed to accelerate deployment of new technologies at scale and to fully implement electricity sector reforms. A robust, market-led system will require additional structural changes if India’s state champions and private companies are to meet the needs of energy-hungry consumers.

Better center and state policy coordination: Improving alignment and coordination between the center and state governments would accelerate decision-making. This would build on progress made in the implementation of policies, such as rural employment guarantees, diesel deregulation and targeted LPG subsidies.

Global oil and gas markets have seen a lot of turbulence since you took over as petroleum minister. How do you think India has managed to navigate through this upheaval?

I took charge of the petroleum ministry in 2021 when the pandemic was in full swing. All strategic decisions we have taken have been done with the prime ambition of making fuels affordable to a population of 1.4 billion. There’s been no shortage of fuels, and our retail prices are amongst the lowest in the world. Today, we are in the situation where India can take reasonable satisfaction in having dealt with the trilemma, which is availability, affordability and sustainability.

India’s decision to boost oil purchases from Russia since the Ukraine war started has drawn a lot of questions. What’s your view?

The decision to buy Russian oil — as well as from other new suppliers — was driven to make fuel affordable to our consumers. Also, global oil prices would have been much higher if India was also competing to buy from Middle Eastern and other suppliers the volumes that it is now buying from Russia. Even as the global transition takes place to green energy, the fact of the matter is that global oil consumption is about 100 million b/d. If two well-known producers are sanctioned — Venezuela and Iran — and if energy coming out of a third producer, Russia, is also taken off, consumption cannot come down overnight. That’s because you’re not going to stop traveling or heating your homes.

In addition to buying oil from Russia, what has been India’s overall crude diversification and supply strategy?

India has not only diversified by buying oil from Russia, it has also been increasing its energy purchases from other major suppliers, such as the US. Today, we buy $20 billion worth of energy products from the US annually. We used to buy oil from about 27 countries a few years ago. Now, we have got to 39, with new sources like Guyana coming up. Except for one or two OPEC producers, the ability of other oil producers to quickly raise output to fill the vacuum is limited. In late 2021, I was told that leading Middle Eastern producers would gradually increase production, which would eventually help prices to cool by February 2022. But then the Russia-Ukraine conflict started. Even now, therefore, whatever cutbacks in production have taken place, the market will have to adjust.

What are the steps India is taking to meet its future energy needs?

Our upstream reforms are all anchored in a sense of pragmatism, farsightedness and an understanding that we require more domestic production. Some of the initiatives include policies to incentivize production in the northeastern region, as well as the decision to open up more sedimentary areas to exploration and production. We are also in the market to acquire more upstream assets and take more equity outside. Because, as I see it, even if we make a major transition to green energy, we will still need oil and gas, at least for another 20 to 30 years. In addition, India is planning to raise its annual refining capacity from the current 250 million metric tons to 400 MMt as refiners increase their capacity to produce more downstream products, such as petrochemicals. Gas is a bridge fuel. We are also slowly but surely moving in a direction where India will be a major producer and consumer of green hydrogen. Our biofuels, ethanol push and biogas plants will be big stories.

Interviewed by Sambit Mohanty, Editorial Lead, Petroleum News at S&P Global Commodity Insights. Sambit is based in Singapore.

Contributor:

Sambit Mohanty

Editorial Lead, Petroleum News,

S&P Global Commodity Insights

sambit.mohanty@spglobal.com

Key trends for India’s power and renewables markets in 2023

India's energy options and the roadmap ahead

Countries face challenge in matching US ‘firepower’ over green industrial policy

US, EU climate policies may pose unforeseen risks for emerging Asian economies

Next Article:

Bigger and Greener: The Changing Landscape of Indian Mobility

This article was authored by a cross-section of representatives from S&P Global and in certain circumstances external guest authors. The views expressed are those of the authors and do not necessarily reflect the views or positions of any entities they represent and are not necessarily reflected in the products and services those entities offer. This research is a publication of S&P Global and does not comment on current or future credit ratings or credit rating methodologies.