The Hydrogen Economy

As the global economy pushes to decarbonize over the next two to three decades, many industries are looking to hydrogen as the fuel to power their energy transitions and meet green production targets. The industrial gas sector is likely to be one of the first to benefit from the move to a hydrogen economy, alongside existing end markets like oil refining, chemicals, and fertilizers.

Published: April 25, 2021

Outlook

The Hydrogen Economy: Hot Air or Future Reality?

The industrial gas sector is likely to be one of the first to benefit from the move toward a hydrogen (H2) economy. They already have much of the infrastructure, and the largest players are already running pilot clean H2 projects that could come on stream by 2030.

Existing end markets, such as oil refining, chemicals, and later on possibly fertilizers, will likely also be among the early adopters of H2. Net zero commitments imply the full decarbonization of hard-to-abate sectors such as steel, but using hydrogen to do so would be extremely costly. S&P Global Ratings therefore sees steelmakers' credit quality as most at risk since the sector's profitability has been weak for years.

Key Takeaways

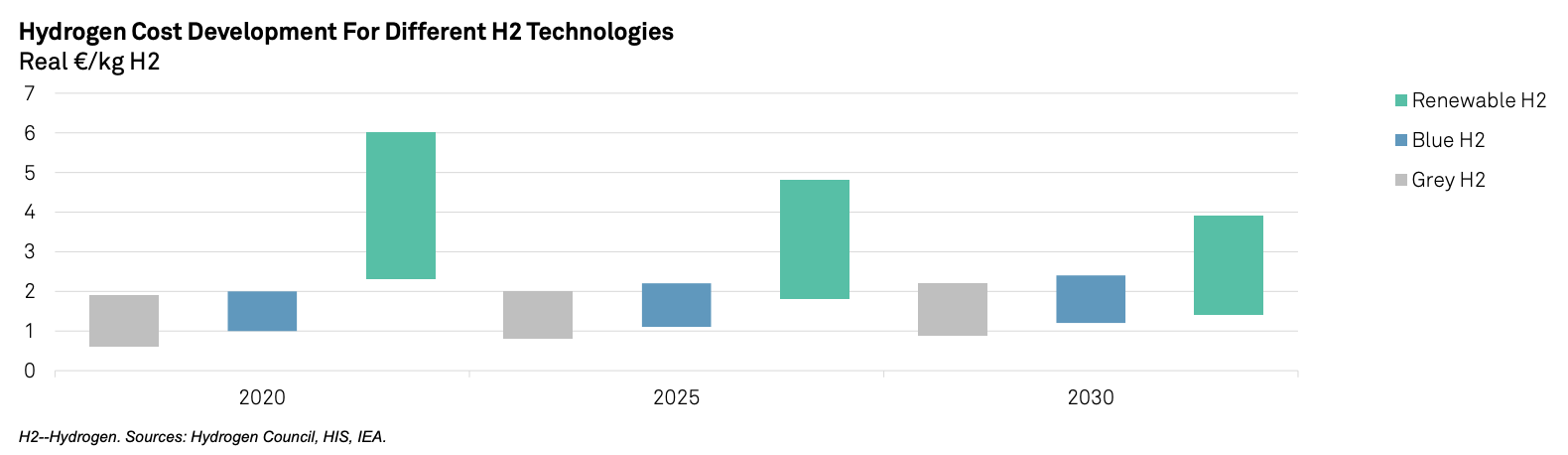

- Hydrogen (H2) is more expensive to produce than natural gas. Whether clean H2 will be widely adopted over the next two decades therefore hinges on supportive net zero policies, a steep decline in production costs from electrolysis,and ample renewables

- Industrial gas players are likely to be among the earliest to benefit from increased outsourcing and demand for clean H2, given their established logistics capability along the hydrogen chain. Existing end markets, such as oil refining, chemicals, and later on possibly fertilizers, will likely also be among the early adopters of clean H2.

- Clean H2 to fuel buses and heavy trucks is a possibility for the second half of this decade,not least because manufacturers will have to adapt to more stringent emission targets in Europe. For autos, S&P Global Ratings does not see hydrogen as the preferred technology because batteries are significantly more energy efficient.

Green Hydrogen

Green H2 Offers Energy and Process Technology Majors A Long-Term Growth Opportunity

As the global energy transition accelerates, rising interest in clean hydrogen means healthy prospects for companies providing technology to energy and utility industries working to meet green production targets.

However, this is unlikely to have an impact on rated capital goods companies' credit profiles before 2025-2030, when construction of the first batch of large hydrogen projects--currently in the planning stage--could commence.

Companies likely to benefit most from the long-term potential include manufacturers of industrial-scale renewable power generation equipment, and engineering groups offering green energy and electrolysis technology-related solutions and services.

The overall net credit impact on the capital goods sector is likely to be positive. That said, the continuous shift away from fossil fuels over the next two or three decades will eventually force market players with high oil, gas, and coal exposure to reconfigure their business models. Already today, the market for new conventional, centralized power generation equipment is suffering from overcapacity, which is bad news for large gas- and steam-turbine producers.

Green Hydrogen May Transform the Fertilizer Industry

The emergence of green hydrogen as a sustainable raw material to produce ammonia, and the potential for ammonia as a store and carrier of hydrogen, could disrupt the nitrogen fertilizer industry, albeit only after 2030.

Read the Full ArticleU.S. Firms Complete Engineering for Green Hydrogen Production Facilities

McDermott International's CB&I Storage Solutions and New Energy Development Company completed engineering for two 50-MW energy projects that can each produce nearly 24,000 kg/day of renewable hydrogen.

Read the Full ArticleExperts Explain Why Green Hydrogen Costs Have Fallen and Will Keep Falling

As electric and gas utilities contemplate investing in low-carbon hydrogen and the technology to produce it, the high price of today's supplies and equipment — and the potential for cost declines — are major considerations.

Read the Full Article

Green Steel

Steel Producers Have A Long Way to Go

The steel industry represents almost 10% of total energy-related emissions globally, and more than 20% in some countries, whether starting from iron ore and coke (consumed in blast furnaces) or scrap metal (using EAFs).

A change to EAFs fueled with scrap or direct reduced iron (DRI) from the traditional high-emission blast furnaces is the most obvious way to reduce emissions in steel production.

Key Takeaways

- For steelmakers, the most feasible way to reduce emissions is to plan raw-material and process efficiencies.

- A technology switch to electric arc furnaces (EAFs) would yield a major reduction in energy intensity and emissions, but requires huge investments that steelmakers can ill afford at the moment.

- Using hydrogen-fueled direct reduced iron for EAFs is even more costly and can only be part of the equation well beyond 2030 in S&P Global Ratings view, if net zero carbon policies provide sufficient incentives and support.

Get the latest news, analysis, and multimedia featuring S&P Global Platts’ insights on hydrogen and its current and future role in the global energy mix.

Access the Topic PageGas

Industrial Gas Companies are In Pole Position

The world's top three industrial gas companies each already earn about $2 billion in revenue from hydrogen business annually, but the rising need for cleaner hydrogen could bring substantial growth.

Industrial users producing their own hydrogen, and planning to switch to cleaner sustainable hydrogen, may decide to increase the amount they obtain externally from the current 10% average.

Can Natural Gas and H2 Have A Symbiotic Relationship?

Hydrogen could ultimately replace hydrocarbons for new fuel cell applications or future power generation.

Read the Full ArticleEurope's Power Giants Send Mixed Messages on Future of Natural Gas

In a strategy presentation in February, Miguel Stilwell de Andrade, CEO of EDP - Energias de Portugal SA, pledged that his company, one of Europe's biggest utilities, would not own any natural gas-fired power plants in 2030, the date by which it wants to reduce its direct emissions to net-zero.

Nuclear

Stick or Twist? Europe Divided on Nuclear Future

With its next generation of nuclear power plants, Europe is aiming to set new standards and herald a nuclear renaissance. But the economics of new nuclear are challenging and European countries have vastly different views on the technology.

Nuclear Plants Could Soon Produce Hydrogen, but Federal Policy Questions Linger

Commercial-scale hydrogen production from nuclear reactors is on the horizon, but its potential deployment will ultimately hinge on federal policies to drive market demand, private sector investment, and infrastructure build-out, experts said.

Read the Full Article'Not Bonkers': Hydrogen Could Give U.S. Nuclear Plants New Lease on Life

Under the right conditions, hydrogen production could offer a lifeline that may prevent some aging U.S. nuclear reactors from retiring early, according to some industry experts.

Read the Full Article

Utilities

Storage Is Paramount for Utilities In the Long Term

Hydrogen is likely to play an increasing role in electricity storage after 2030 for U.S. and European power utility companies, notably if and when renewables account for the majority of power output. Hydrogen-fueled power generation will remain expensive compared with gas, in S&P Global Ratings view, and is therefore unlikely to play a role in baseload, but its value may lie in providing clean dependable capacity for peak loads.

Keeping gas capacity--even at low load factors--may remain important for supply security and affordability.

How One of Europe's Dirtiest Utilities is Planning to Decarbonize

Bełchatów Power Plant, located near its namesake town in central Poland, about 100 miles southeast of Warsaw, is a structure of superlatives.

Read the ArticleNational Fuel's Gas Utility Envisions Dedicated Hydrogen Systems, Hybrid Heat

A pathway to decarbonizing National Fuel Gas Co.'s gas utility is coming into focus for executives, and while it could involve selective building electrification, it remains rooted in the business of moving molecules.

Read the Full Article

Electric Vehicles

For Light Vehicles, Hydrogen Is Not for this Decade

Skeptics who said electric vehicles (EV) would never be widely accepted have been proved wrong. With a balanced cocktail of punitive environmental regulation and generous public incentives, authorities have shown it is possible to stimulate strong demand. In Europe alone, EVs already increased to more than 10% of total passenger vehicles sold in 2020, compared to less than 4% just the year before.

Key Takeaways

- S&P Global Ratings expect hydrogen to play a limited role in decarbonizing global light-vehicle mobility this decade and it is unlikely to influence auto manufacturers' credit quality.

- Despite concerns about their range and durability, battery electric vehicles currently offer far superior energy efficiency than hydrogen fuel cell vehicles.

- Beyond 2030, the phase-out of combustion engines, scarcity of materials for battery manufacture, and government policies could support hydrogen as an alternative decarbonization technology for light vehicles.

- Hydrogen may, however, have prospects for heavy trucks and commercial vehicles this decade given weight and range considerations and tightening CO2 emission targets in the EU from 2025. Some manufacturers have cautiously established exploratory joint ventures and partnerships.