Commercial real estate in the US is experiencing a confluence of challenges – including secular shifts in demand, the adoption of hybrid work, higher borrowing costs and volatile capital markets, and turmoil in the banking sector.

S&P Global Market Intelligence's June 2023 Commercial Real Estate Chart Book: Weathering the Storm brings together a wide range of resources updated through the first quarter. The chart book highlights bank regulatory data, loan-level and aggregate US life insurance company disclosures, information on individual commercial properties and key metrics of portfolio performance and valuation for real estate investment trusts, to provide additional context on the breadth and scope of commercial real estate exposure across financial institutions sectors.

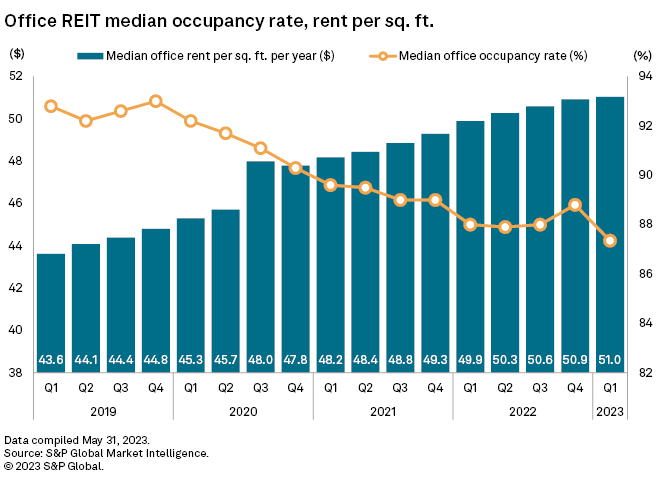

Read MoreMore than half of US office real estate investment trusts began 2023 with mostly weaker quarterly operating metrics during the first quarter, according to an S&P Global Market Intelligence analysis.

Operating funds from operations (FFO) for 12 office REITs dropped quarter over quarter, while eight REITs booked sequential gains during the first quarter.

The proportion of gains and losses among office REITs was almost the same when looking at recurring EBITDA, with 11 REITs logging quarterly losses, as opposed to 10 REITs that reported gains.

Read the Full Article

Inflation and rising interest rates are taking a toll on European commercial real estate (CRE). CRE companies and commercial mortgage-backed securities (CMBS) continue to struggle with refinancing debt maturities, with CRE transactions happening at a slow pace and a smaller size. Even so, European banks' CRE exposure increased by 2.3% between the fourth quarter of 2022 and 2021 and contributed to an almost 1% rise in their loans to non-financial corporates in the same period.

Read the Full Report

Take Notes is joined by credit analysts Casper Andersen to discuss how covered bonds could ease the pain in European commercial real estate (CRE), which has been struggling with inflation and rising interest rates. First, we go into the price trends of different CRE segments. We touch on covered bond rating performance. Finally, we talk about the potential for covered bond funding, which varies significantly depending on the covered bond issuer and jurisdiction, and green covered bonds, which may offer a potential source for further CRE funding.

Read MoreThe Federal Reserve's aggressive monetary policy tightening in the face of nagging inflation, combined with secular shifts in CRE (particularly in the office sector), are heightening refinancing risks for many borrowers and the strains won't likely ease any time soon.

Pressures on credit quality for rated REITs and CMBS look set to persist for at least the next one to two years, as declining demand dampens rental growth and occupancy rates while borrowing costs escalate. This comes as turbulence in the banking sector further strains financing conditions, given that U.S. banks account for the bulk of CRE lending.

Read the Full Report

In the wake of the failures of three sizable U.S. banks, market sentiment toward the banking industry is somewhat fragile. The steep increase in interest rates has also raised concern about the health of banks' commercial real estate (CRE) exposures. So far, bank credit costs have remained relatively benign, with only a modest uptick in provisions and allowance for loan losses in the first quarter. S&P Global Ratings expects credit costs to rise throughout this year--by how much will depend on the depth and duration of a potential recession. S&P Global Ratings' economists expect a shallow recession in the second half of the year but have also raised the chances of a harder landing.

Read the Full ReportSome US banks greatly expanded their exposure to commercial real estate loans in recent months as a result of M&A transactions.

Commercial real estate (CRE) loans at US banks rose to $2.436 trillion as of March 31, up 0.54% from $2.423 trillion at the end of 2022. On a year-over-year basis, CRE loans were up 10.51%.

Among CRE loan types, only multifamily loans declined, falling to $593.09 billion as of March 31 from $598.40 billion at the end of 2022. Construction and land development loans, nonowner-occupied nonresidential property loans, and CRE loans secured by collateral other than real estate all rose from their year-end 2022 totals.

The commercial real estate (CRE) industry is not only facing slowing growth and higher funding costs but also headwinds from volatile capital market conditions and tightening access to capital. Banks remain the main lenders to CRE companies, accounting for 50% of total loans outstanding, with regional banks having an outsized exposure. The recent turmoil in the banking sector could further tighten access to credit as banks have been pulling back from new CRE lending amid concerns about credit quality. Banks' unwillingness to extend or amend loans as they mature could increase the refinancing risk for maturing debt in the next year.

Growing interest among US banks in selling commercial real estate loan portfolios has not yet translated into a wave of deals despite a large pool of potential purchasers — in part because buyers and sellers are not finding common ground on pricing.

Read the Full ArticleUS banks with large commercial real estate loan concentrations must work to proactively mitigate any potential problems or run the risk of regulatory intervention.

As concerns over commercial real estate (CRE) grow and those portfolios face headwinds, regulators have made it clear they are paying extra attention to banks with outsized concentrations and will not shy away from taking action against institutions that present risk. Those actions could include regulatory rating downgrades and increased capital retention requirements, experts told S&P Global Market Intelligence. Banks should take steps now to mitigate risk in order to avoid such actions, they said.

Read the Full ArticleThe aggregate HVCRE loan balance for US banks stood at $32.37 billion in the first quarter, down from $41.39 billion in the fourth quarter of 2022, and $34.29 billion in the prior-year period, according to S&P Global Market Intelligence data. This marks the lowest balance of such loans since the first quarter of 2019.

Read the Full Article