Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

Deglobalization as a geopolitical risk

The years ahead will be defined by a set of shared challenges - climate risk, making the energy transition, disruptive technology and cybersecurity, inequities, and pandemics.

Yet, the continued growth of global trade has raised questions for countries and businesses, including around the risks of interdependence. Globalization – in which macroeconomic forces, trade policies, and global supply chains link countries and corporations closer together across borders – is being reconsidered due to policy, security, and economic issues. As a result, many governments, business and civil actors are considering the value of moving toward a more insular approach to trade and commerce as countries look to position themselves in a rapidly changing landscape. This shift – sometimes known as “deglobalization”, represents a developing geopolitical risk for businesses.

One of the significant drivers of the deglobalization movement was the 2008 global financial crisis. In response to global economic instability, some governments refocused their policies and rhetoric around protectionism, introducing limits to the free flow of trade and investment across borders.

Recently, protectionist policies have been fueled by the global pandemic and Russia’s invasion of Ukraine. Following the invasion, 24 countries implemented export bans, covering basic foodstuffs such as wheat, sugar and oils, according to the International Food Policy Research Institute.

Acute supply chain disruptions and rising protectionism have fueled fears of shortages that, have led governments to consider strategies such as reshoring (bringing their supply chains home), nearshoring (building supply chains with their neighbors) and friendshoring (trusting their supply chains to their allies). Governments are also pursuing industrial policies in the wake of recent geopolitical developments. Both the US CHIPS and Science Act, passed in 2022, and the European Chips Act, approved in April, were triggered by the global semiconductor shortage, and seek to ensure adequate production of US- and EU-made chips for domestic manufacturers – even when homegrown technology is more costly than imported supplies.

Multidimensional social challenges have contributed to the debate over globalization and its effects. The emergence of interconnected, country-level risks has forced businesses to reconsider how to operate in a post-pandemic world. These risks include climate risk, economics and inflation, international security, COVID-19 recovery efforts, trade flows and access to credit.

While the debate around deglobalization is likely to persist, S&P Global Market Intelligence’s data, including vast trade intelligence, forecasts a return to a long-term trend of growth in global trade in the years ahead.

<span/>At this point, deglobalization is more of a point of rhetoric than an economic trend. However, the risks of deglobalization are real, and substantial.

Economics of deglobalization

While some countries benefit economically from globalization, there is growing awareness that global development remains uneven. The increased inequality between countries has created negative effects on social and political stability. Economic indicators such as GDP, inflation rates and business activity can help us understand how globalization could drive economic growth worldwide.

Some markers of deglobalization include:

- Increased trade barriers such as tariffs and quotas.

- Reduced foreign direct investment (FDI).

- Localization of global supply chains.

- Increased regulation.

- Increased geopolitical tensions.

The following sections examine recent economic trends to gauge how globalization has affected certain countries.

Overall economic health: GDP upside surprises

India has seen significant economic growth over the past few years that some observers have linked to its increasing popularity as a hub for multinational corporations. Multinationals from various sectors have shown increased interest in India, with FDI inflows hitting an all-time high of $85 billion during fiscal 2021-22. India’s economy grew steadily in 2022, according to estimates from the country’s National Statistical Office, with a real GDP growth rate of 7% for fiscal 2022-23.

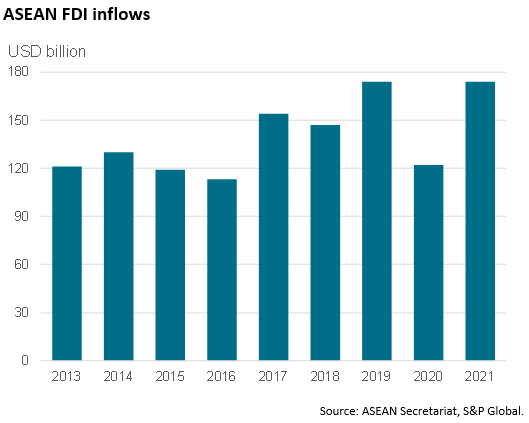

Association of Southeast Asian Nations FDI inflows

The graph above shows the Association of Southeast Asian Nations foreign direct investment, which reached a record $174 million in 2021, owing largely to investments in electronics manufacturing, electric vehicle manufacturing and EV battery plants.

Global inflation and its drivers

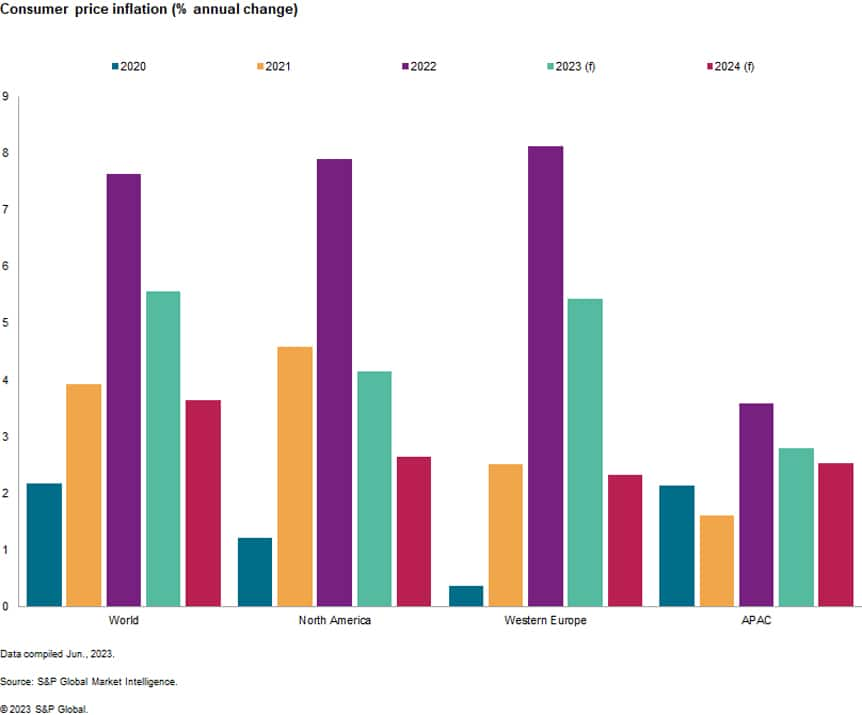

Global inflation rates reached multi-decade highs in 2022 but is expected to moderate in response to tightening financial conditions. S&P Global economists believe that this is mainly due to rebalancing supply and demand levels and COVID-19-related policies. In 2022, the global consumer price index inflation rate unexpectedly soared, surpassing an initial assessment that the pickup would be transitory. There are different interpretations of the cause of this inflation. Some economists believe it was caused by excessive financial stimulus by governments related to COVID-19, while others believe it was caused by supply chain failures that drove up the prices of goods and raw materials. Still others attribute inflation to energy costs following Russia’s invasion of Ukraine. The COVID-19 pandemic caused the global consumer price index inflation rate to slip in the fourth quarter of 2020, but by the fourth quarter of 2021, it jumped to 5%, peaking at over 8% in the third quarter of 2022 after Russia’s invasion of Ukraine.

Chart 1: Consumer price inflation (%)

Growth rebounds in the G4 economies

After seven months of decline, business activity in the G4 economies of the US, eurozone, Japan and UK rebounded in February, according to a weighted average of the headline Purchasing Managers’ Index (PMI) composite output index for the four markets. The index rose for a second month, from 48.5 in January to 51.3 in February, breaking through the 50.0 no-change level.

This is an encouraging sign of broad-based improvement, with growth recorded in all four economies for the first time since June 2022. The US and UK reported growth for the first time in eight and seven months, respectively, while the eurozone grew for a second successive month, with the rate of expansion accelerating to its highest level since May 2022. Japan also eked out modest growth for the second month in a row.

<span/>Solutions to manage through geopolitical risk

Negative impact of reduced trade flows

Global trade flows of goods and services have facilitated economic growth in the past few decades, but more recently, protectionism and pandemic-related restrictions have cast global trade flows in a negative light. This reduction impacts employment, economic growth and productivity and lowers the rate of innovation and investment.

The slowdown in trade observed in the second half of 2022 is expected to continue into 2023. The latest GTAS Forecasting model estimates that 2023 trade volume growth will essentially be flat, with value growth estimated to reach about 1% year on year before returning to long-term growth trends from 2025.

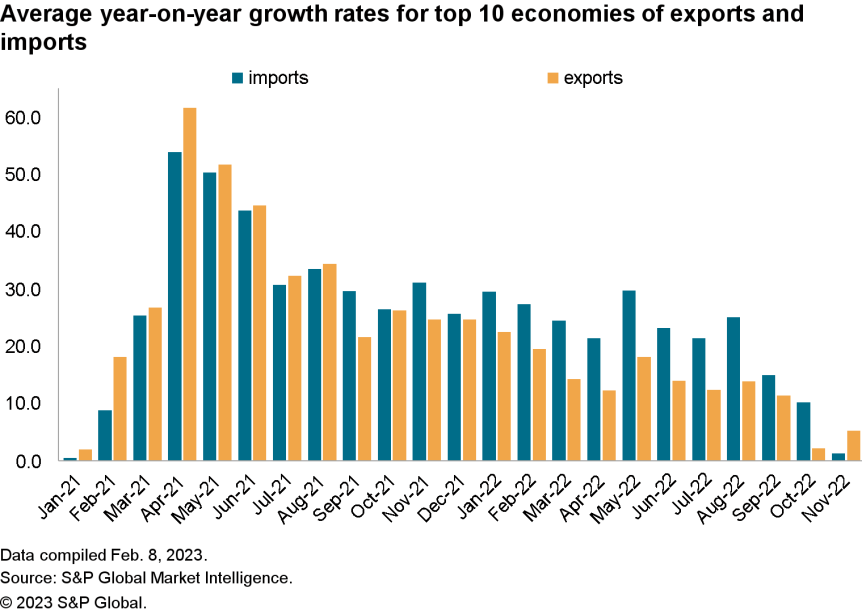

In November 2022, the average year-on-year growth rates for export and import value among the top 10 countries reached 5.2% for exports and 1.3% for imports. Mainland China, Japan, South Korea, Canada and the US slowed down in terms of exports, with mainland China experiencing the most significant drop of 9.2% year on year, while India, Brazil and the UK experienced the highest growth rates for exports.

Average year-on-year growth rates for top 10 economies of exports and imports

Mainland China experienced negative year-on-year growth rates for exports and imports in October, November and December 2022, but its easing of COVID-19 restrictions is paving the way for a stronger-than-anticipated economic recovery. There are already signs of economic normalization, and while overseas demand weakens, domestic demand supported by government policies is expected to lead the recovery in mainland China.

<span/>A decline in the automotive and consumer goods trade may be offset by the machinery and electrical goods trade. This would be reflected in national-level performance, with growing exports from China and South Korea outpacing Japan’s downturn while EU and US imports fall. The GTAS Forecasting model projects global trade activity in real terms to fall by 1.9% year on year in the first quarter and by 1.4% in the second quarter, before recovering later in 2023 to reach 0.6% overall growth for the year.

Get in-depth credit coverage

Global supply chain headwinds

The COVID-19 pandemic and geopolitical tensions have created significant challenges for global supply chains. Although supply chains have improved, showing signs of normalization, they have not recovered to their previous level of efficiency. The flash PMI data for February 2023 on global supply chains showed that average supplier delivery times in the major developed economies fell in early 2023, facilitating higher output and moving pricing power from suppliers to buyers. This is having a positive impact on inflation by pushing down industrial prices.

Despite this, there are still concerns over the speed of deliveries. Suppliers have been able to supply inputs to factories due to lower demand. With a drop in new orders, manufacturers reduced their input buying in early 2023 to one of the lowest levels seen in the past decade. Manufacturers and suppliers are focused on reducing inventory levels by shipping goods to customers faster than before, and often by offering reduced prices. However, this is not a sign of broader economic health as it indicates a focus on reducing inventory rather than meeting actual demand.

<span/>Manufacturers also reported the slowest rate of input cost inflation in two years. However, the larger picture is worrying since lower input cost inflation may indicate reduced demand rather than improved global supply chain efficiency.

International security: deglobalization vs. globalization

The geopolitical order has become more precarious as tensions between nations rise, creating geopolitical risks that threaten global trade. The US and China have imposed restrictions and duties on each other’s products. Despite expressing a willingness to continue negotiations and work toward a more comprehensive trade deal, many tariffs on both sides remain in place.

Although the US and China have agreed to collaborate on global issues such as climate risk and trade, the relationship between the two nations remains complex. How that relationship evolves in the coming years will have far-reaching effects on the movement toward deglobalization. Unresolved issues around trade create an uncertain and unstable environment that is not conducive to global markets.

Europe’s short-term security

Russia’s invasion of Ukraine in 2022 upended the economic stability of Eastern Europe, disrupting the region's trade, economics and energy flows. This has led to a renewed focus on energy security and a potential retreat from globalization as countries look inward to prioritize domestic resilience over international trade.

The geopolitics of the oil market in particular have become more contentious, with government decisions in Beijing, Brussels, Moscow, Riyadh and Washington, DC, shaping oil prices and oil flows. The US and the EU have imposed aggressive sanctions on Russia’s energy industry, while the lifting of COVID-19 restrictions in China will play a crucial role in determining the demand growth for oil in the coming years.

The sanctions imposed on Russia by the EU, US and their allies have implications for the global energy market. The Group of Seven (G-7) countries have imposed economic sanctions on Russia, and the EU has introduced price caps on Russian natural gas, leading to a tight energy market in the short term. This has resulted in elevated gas prices in Europe, which are expected to remain high throughout the winter of 2023-2024, before declining thereafter. Additionally, global oil prices are projected to rise to $110 a barrel in 2023-2024, before falling to an average of $85/b in 2025.

Russia's invasion of Ukraine has also forced countries outside of Europe to confront global risks such as nuclear proliferation, cyber operations, infrastructure resilience and the future of security alliances.

Learn more about credit estimates

How the COVID-19 pandemic helped fuel the deglobalization movement

The COVID-19 pandemic significantly raised scrutiny on globalization and international cooperation. With disruptions to global supply chains and economies worldwide, the pandemic has highlighted the potential to diversity exposures and vulnerabilities of relying too heavily on other countries for essential goods and services. This has resulted in the acceleration of the conversation around deglobalization, with many countries declaring an intent to focus on building up their domestic capabilities and reducing their dependence on foreign sources.

<span/>At the same time, the COVID-19 pandemic also highlighted the need for global cooperation and solutions. This has led to the reorganization of global priorities, structures and relationships, with countries adopting a more pragmatic approach to addressing social and economic challenges in the post-pandemic world. This effort involves balancing mutual interests with national interests and fostering cooperation while also vying for economic and political superiority.

Credit ratings in deglobalization

The risks and challenges associated with deglobalization could have wide-reaching commercial impacts. With the world experiencing a new era of uncertainty and instability, businesses and markets must navigate sanctions, government interventions, increased protectionism, reputational risks and alternative payment systems. This new era is characterized by geopolitical risks such as war in Europe, an energy crisis, high inflation, a slowing global economy and political tensions between major players. These geopolitical risks threaten to weigh on businesses and markets, but there are early signs that some of the pressure is easing, providing hope that credit conditions could stabilize in the second half of 2023.

<span/>The availability of credit has become a top priority for countries and businesses in the context of deglobalization. Instead of engaging in competitive international trade markets, companies must rely on regional sources, which can result in higher costs and in difficulties securing funding. S&P Global Ratings expects the pressures on credit ratings to intensify in the near term as corporate borrowers find it more challenging to pass high input costs on to consumers who are struggling with rising prices and mild recessions in some of the world's largest economies. Speculative-grade corporate default rates in the US and Europe are forecast to double as central banks in the developed world remain hawkish to fight inflation, and governments have fewer fiscal options to deploy after piling on debt during the pandemic.

Understand the Europe-Africa trade and investment relationship in the three- to five-year outlook.

Conclusion

In recent years, the debate over deglobalization has increased in volume due to political, social and economic developments. The 2008 global financial crisis led many to question the benefits of globalization, and some governments began to adopt protectionist policies. The rise of anti-globalization rhetoric has fueled this trend, as have multidimensional social and environmental challenges, including climate change, international security and the COVID-19 pandemic. The near-term reduction in trade flows has negatively affected employment, economic growth and productivity, which has lowered the rate of innovation and investment in industry. Although the global economy shows signs of resilience, with declining global inflation rates and rebounds in the G4 economies, it remains to be seen how the trend toward deglobalization will evolve in the years ahead.

<span/>Related deglobalization research and analysis

Looking for deglobalization related solutions?

Understanding global credit

Learn the difference between Foreign Currency Credit Ratings and Local Currency Credit Ratings with S&P Global Ratings.

Solutions to manage through geopolitical risk

<span/>Protect your investments with S&P Global's Country Risk. Speak with a specialist today.

Strategic sourcing and footprint analysis

Gain competitive advantage: evaluate risks & opportunities in strategic sourcing.