Minus Nine Now

In CRISIL Research's May 26, 2020, GDP outlook, India’s worst recession in decades was at hand. Come September, CRISIL now foresees it contracting further by a rate not seen since the 1950s. GDP growth in fiscal 2021 will dive deeper as risks coalesce.

Published: October 8, 2020

-

COVID-19

The Viral Drag

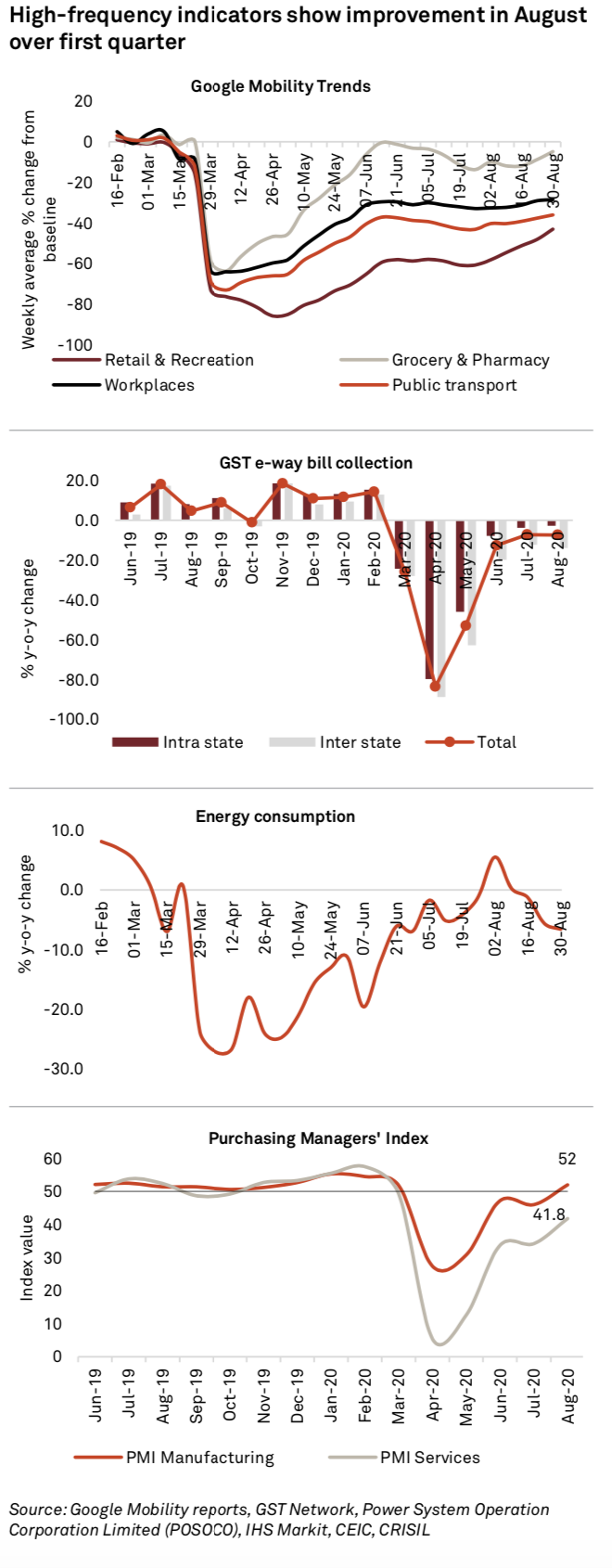

CRISIL cut through the clutter to analyse four important metrics related to the pandemic – the number of daily cases reported, the rate of recoveries, the state-wise patterns, and the rate of growth in new cases (India and state-wise).

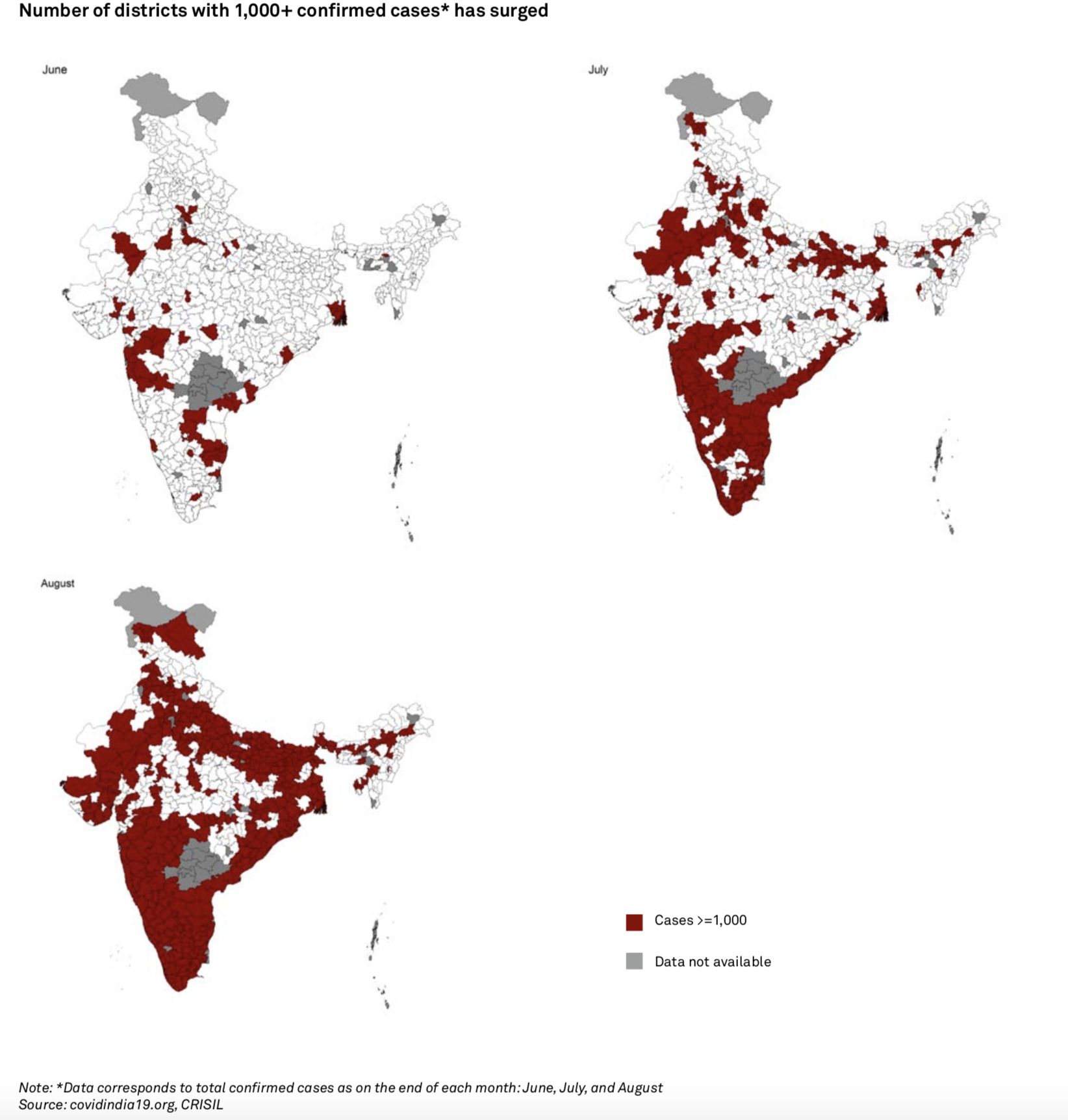

The number of confirmed Covid-19 cases in India crossed 42 lakh as on September 7. In the last week of August, India reported ~5 lakh new cases and the highest numbers of new cases globally. Early predictions by various agencies of the number of cases in India peaking in the early part of the July-September quarter have come to a naught. Even if recoveries have risen to 77.3% as on September 7, the daily rise in cases continues to surpass the daily number of recoveries. Globally, too, the virus is rearing its head again, with Japan, South Korea, Europe and Hong Kong, seeing new cases lately.

Key Takeaways:

- Presence of asymptomatic infections suggests the numbers of Covid-infected patients in India is higher than reported.

- Industrial and service sectors, accounting for ~85% of GDP, suffered the most because of the nationwide lockdown, as shown in the first quarter GDP data.

Rural India

Reading Rural Demand

Agriculture was the only major sector that registered positive growth in the first quarter of fiscal 2021 – a sole bright spot. But that is only part of the rural story, as non- farm activities contribute a much larger chunk. As per NITI Aayog, agriculture’s share in the rural economy was only 39.2%. Hence, what happens to the non-farm sector is equally or more important.

Key Takeaways:

- Agriculture was the only major sector that registered positive growth in the first quarter of fiscal 2021 – a sole bright spot.

- As per NITI Aayog3, agriculture’s share in the rural economy was only 39.2%.

- Other than healthy agricultural growth, front loading of government expenditure under its various rural focussed schemes in the wake of the pandemic likely led to the above trends. It remains to be seen however, if the momentum sustains going ahead.

- But while retail food inflation is rising, the farmer is not benefitting proportionately as wholesale inflation – a better indicator of what farmers’ incomes would be - remains soft.

Capital

The Slack in Consumption and Investments

Private final consumption expenditure (PFCE), or consumption expenditure of households, and gross fixed capital formation (GFCF), or investments, are the largest and second largest demand side components of the Indian economy, respectively. Their shares in GDP in fiscal 2020 were 57.2% and 29.8%.

The pandemic only magnified the pre-existing weakness in private consumption and investments. While GFCF was falling even before the pandemic, PFCE growth turned negative for the first time, in the new (2011-12) GDP series. The fall in GFCF has been much steeper than that in PFCE. Despite some support from the rural economy, private consumption is expected to sink this fiscal. A rising number of cases in rural areas could complicate and delay return to normalcy. This means continued uncertainty about employment prospects and incomes.

Consumption of some services, especially contact- based such as travel, sports and entertainment will also remain muted till such time a Covid-19 vaccine is mass produced. High retail inflation at a time when incomes are falling, is a double whammy to disposable incomes.

{kind=link}

The Funk in Investments

- Capacity utilization has been below 70% since the September 2019 quarter (the latest print was 69.9% for March 2020). This has likely fallen further, given the large-scale demand destruction in the economy.

Financial Pulse

Financial Conditions Ease, but Ailments Linger

Monetary policy has done most of the heavy-lifting so far in supporting the economy. This was needed since financial conditions had seen a severe tightening in India and via spillovers from rest of the world. Recent months have shown that RBI’s monetary easing, coupled with improving global sentiment, helped ease financial conditions. However, some segments of the financial sector are facing growing stress fundamentally, which could bite back once the excessively easy monetary policy normalises.

Key Takeaways:

- FPI flows have returned and exchange rate has stabilised, even appreciating in the past 2 months.

- The sharp rate cuts – totalling 115 bps since March 2020 – coupled with regulatory relief for corporates contributed to a rally in stock markets.

- According to a recent analysis by CRISIL Ratings5, 2,300 companies out of CRISIL’S total rated universe of about 8,000 corporates availed of moratoriums.

- 75% of these 2,300 corporates have sub-investment grade ratings (rated BB+ or lower by CRISIL).

- Despite 10-year G-sec yields easing, their term premium over repo rate remains stubbornly above 100 bps, reflecting the fiscal risks factored in by investors

Planning Recovery

The Scars and the Way to Heal

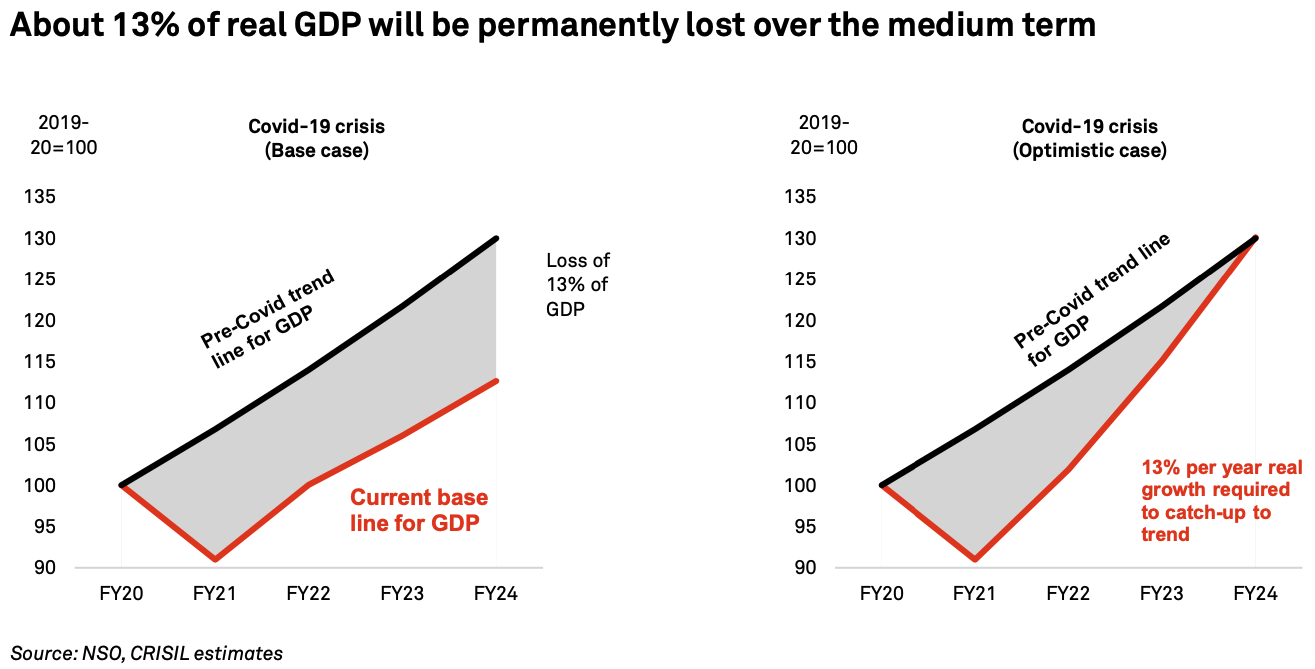

S&P Global foresees, on average, a 3% permanent hit to GDP in Asia-Pacific economies (ex-China and India) over the medium run. For India, however, we estimate the permanent loss at 13% of real GDP.

Key Takeaways:

- De-globalisation, which started with the global financial crisis of 2008, and further fed by the US-China trade wars, is all set to accelerate with the pandemic.

- To balance the near and medium term growth concerns, the government needs to take more steps to address the current pain in the economy.

- The medium term growth path for India is likely to trend down in the business-as-usual scenario.

- n the base case, we see growth shooting to 10% in fiscal 2022, on the back of a very weak base and some benefit from the rising-global-tide-lifting-all- boats effect.

Further Reading

More of our coronavirus coverage

– COVID-19 is Taking a Bite Out of Food Supply Chains – ESG in the Time of COVID-19 – Oil Markets in Crisis Special Report – Special Report from S&P Global Ratings – Research from S&P Global Ratings – Latest news from S&P Global Platts – Insights from S&P Global Platts – Research from S&P Global Market Intelligence – All division coverage from S&P Global